Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

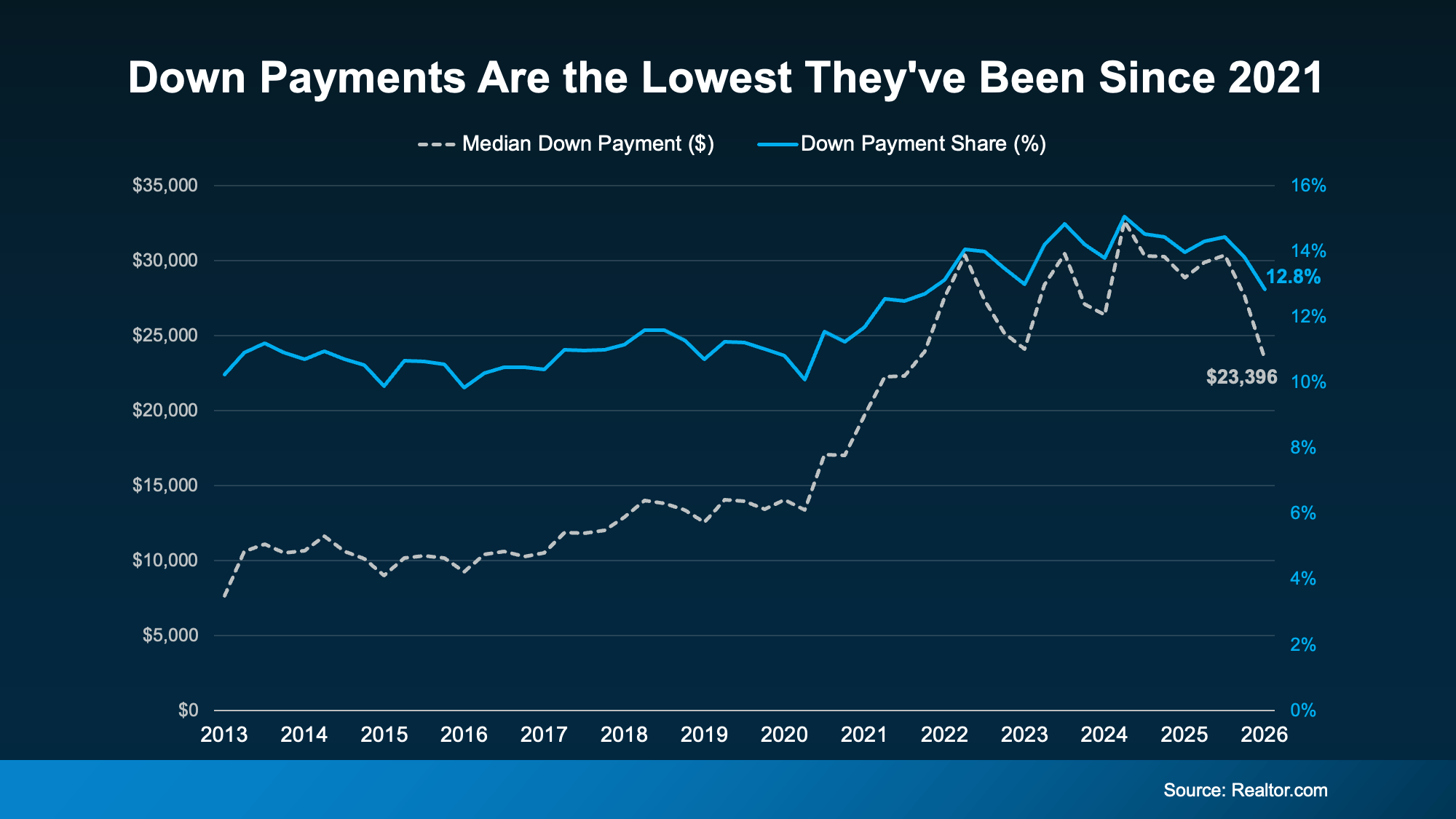

Down Payments Are Smaller Than They’ve Been Since 2021

Saving for a down payment can feel like the hardest part of buying a home. And with affordability as tight as it’s been lately, it’s fair to wonder how anyone manages it right now. Here’s something you may not have seen coming.

Some people are getting their foot in the door with a smaller down payment.

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s around $5,000 below what was typical the year before (a 19% drop year over year). That’s the lowest down payments have been since 2021 (see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

- Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

- More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

- Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

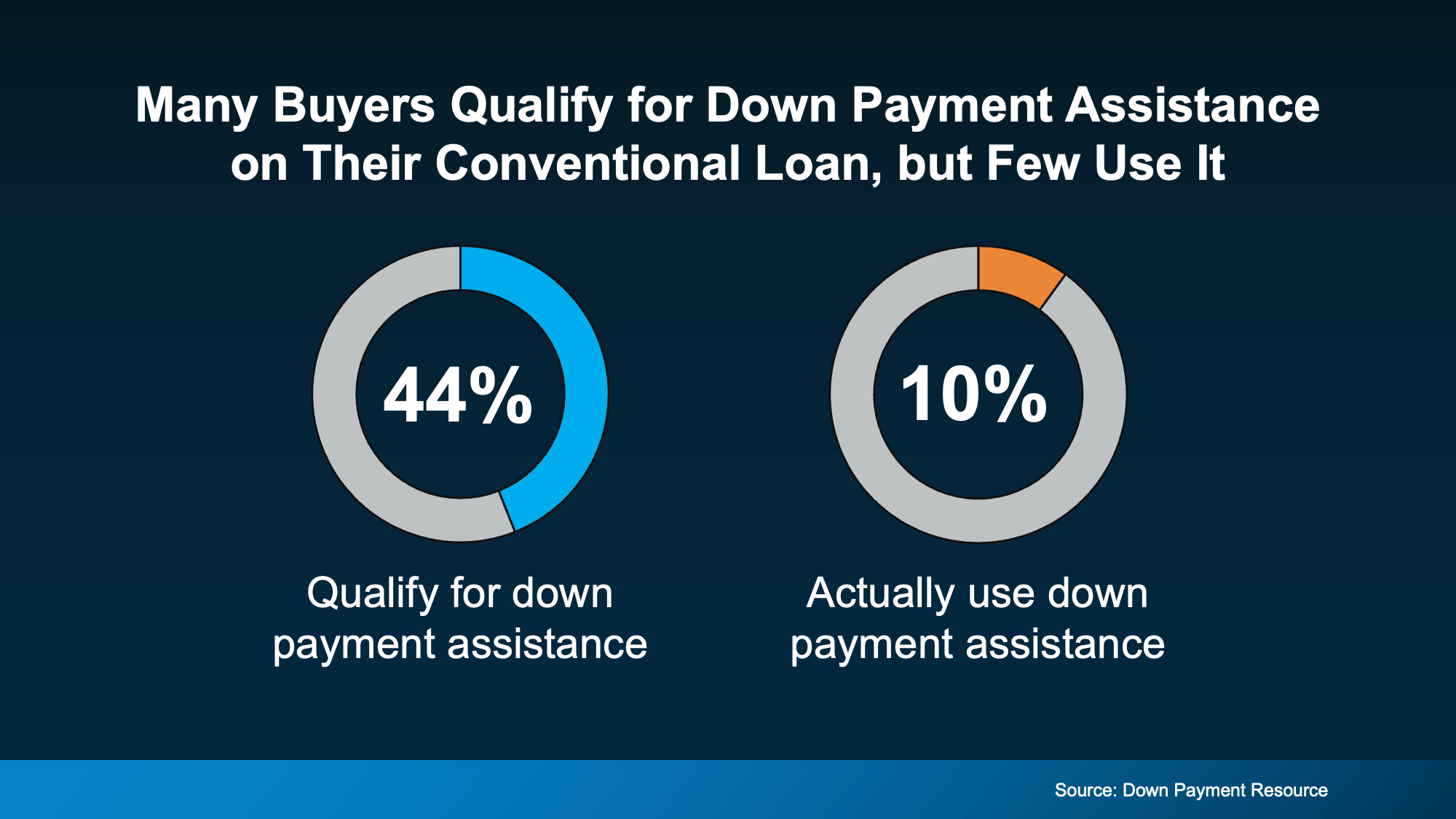

Help You May Not Know You Qualify For

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

- There are more than 2,600 down payment assistance programs available

- More than half (62%) are designed to help first-time buyers

- 38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

- 62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized. Connect with a trusted lender to talk through your options.

![]()

(928) 458-4025

The Mid-Year Housing Market Update: Why Forecasts Changed in 2026

If the housing market feels confusing right now, you’re not alone.

Mortgage rates have risen. Home sales haven’t picked up like expected. And many buyers and sellers are wondering when things are going to feel easier or be more affordable.

The truth is: a lot changed over the first half of this year.

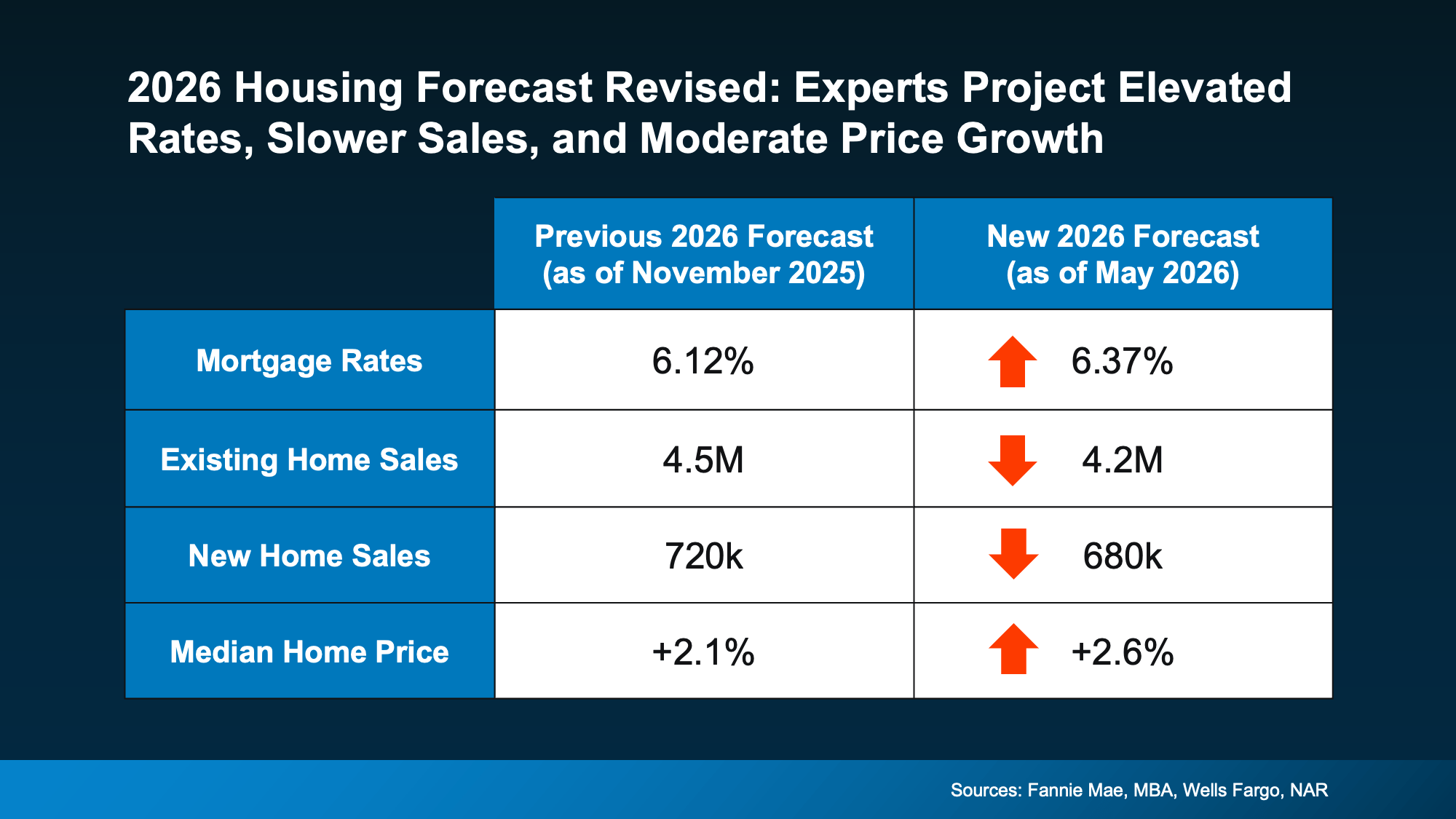

Back at the end of 2025, economists were forecasting a much stronger housing market for 2026. They expected mortgage rates to come down, affordability to improve more dramatically, and home sales to rebound.

But lingering inflation, economic uncertainty, and growing geopolitical tensions overseas pushed mortgage rates higher than expected. And because rates stayed elevated for longer, many buyers continued to hold off.

That’s why experts recently revised their housing forecasts for the rest of the year (see graph below):

So, what does this actually mean for you? Let’s break it down.

Mortgage Rates May Remain Elevated

While just about everyone wants mortgage rates to go back to the uppers 5s or low 6s we saw at the start of the year, as of right now, the experts don’t think that’s likely to happen this year.

Instead, forecasts have been updated from the low 6s they originally projected. Many industry organizations are saying rates will stay in roughly the mid 6s this year. The good news is, that’s still lower than rates were a year ago.

Of course, this is based on what we know today. If the conflict overseas comes to an end or inflation drops, this could change. But if you’re waiting for lower rates, it may not pay off in the way you expect.

Existing Home Sales Revised Lower

Back in late 2025, experts expected we’d sell an average of 4.5 million homes this year. Now? That’s dropped down a bit to 4.2 million.

That tells us something important: buyers are still hesitant because affordability remains challenging.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. And that’s slowed the pace of the market compared to what was originally expected. But even though the forecast was revised down, we’re still expected to sell more homes than last year.

Once geopolitical tensions resolve and rates begin to settle down, many experts believe that group of buyers will be ready to jump back in. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

There has already been a few glimmers of renewed hope lately. In recent months, pending homes sale have been improving month-over-month despite higher rates.

So, if you’re able to afford a home at today’s rates, it could still make sense to buy now. Because otherwise, if you wait, you’ll have more competition (and potentially fewer homes to choose from) when those others buyers jump back in.

New Home Sales Also Slowed

Builders also expected to have a stronger year. Earlier forecasts projected new home sales would top 700k in 2026. Now, economists expect we’ll be just shy of that number.

Again, mortgage rates are a major reason why.

But the upside for buyers is that builders may be even more motivated to sell. That means builder incentives, negotiation opportunities, and pricing flexibility may continue in many markets. So, if you live somewhere where there’s more new construction, this may actually be a bright spot for you.

Builders could be more ready to negotiate, and that gives you more leverage to get a better deal.

Home Prices Are Still Expected To Rise

This is one of the most important takeaways from the entire forecast. Even though sales activity is slower, on average, experts did not revise their home price forecast downward.

They still expect prices to rise nationally this year.

Why? Because while buyer demand has softened, the number of homes for sale is still relatively limited overall. That imbalance is helping support prices, even in a slower market.

Of course, conditions vary depending on where you live. Some markets are cooling more than others. But nationally, experts are still projecting steady price growth — not a major decline. And that should be a comfort whether you’re buying or selling.

Because sellers don’t want a major drop in prices. And while buyers may think they do, generally you feel better about a big purchase when it doesn’t depreciate right away.

Bottom Line

The housing market hasn’t rebounded as quickly as experts originally hoped. But that doesn’t mean it’s stalled.

Higher inflation and lingering economic uncertainty caused economists to revise their forecasts for this year. But importantly, when those two things settle down, many experts believe the market will regain its momentum.

So don’t see this revision in forecasts as a sign of trouble. See it as a temporary reaction to overall conditions and uncertainty.

If you want to know what’s happening in our local market, and what it could mean for your plans for the rest of this year, let’s connect.

![]()

(928) 458-4025

The Secret To Selling Fast, No Matter the Market

When you put your house on the market, you don’t just want it to sell. You want it to sell fast. But the thing is, nationally, it’s taking a little longer to sell lately. And that slowdown can feel frustrating if you want a fast process. Here’s what you need to realize.

In every market right now, there’s one clear exception:

Well-priced, well-presented homes are still selling, and it’s often faster than you’d expect.

If you can tap into that, you can still set yourself up to move quickly, too. Here’s how to get it done.

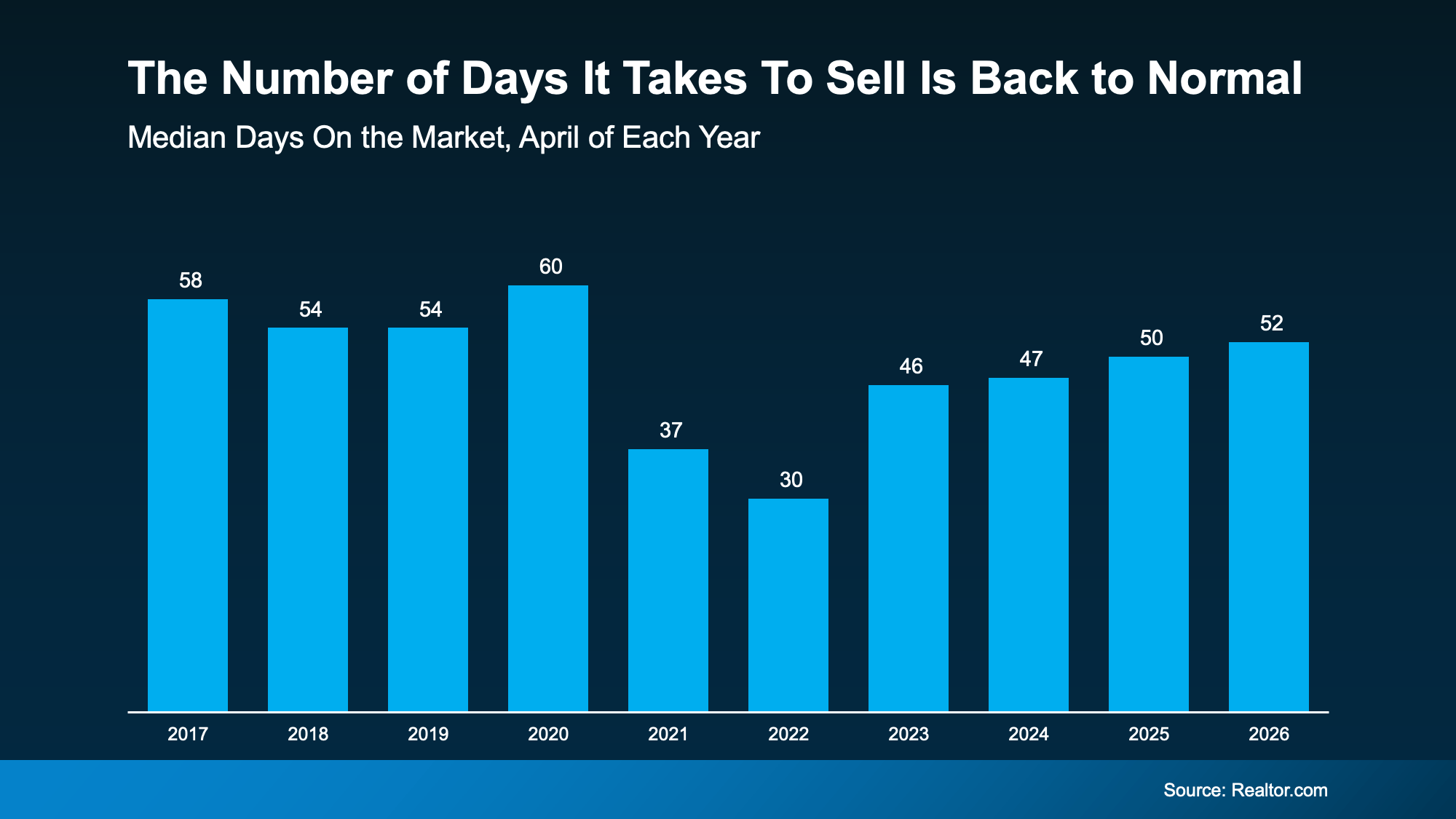

How Long It Takes To Sell Today

According to Realtor.com, homes are selling in about 52 days right now. That’s how long the process takes from the day it hits the market until closing day.

And while that may sound slow to you, it’s not slow. It’s normal.

That’s because it’s pretty much right in line with what it was during the last normal years in the market (see 2018-2019 in the graph below):

It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly.

It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly.

But here’s what matters most. The market is normalizing. Not at a standstill.

This is the norm for timing from start to finish. You may have an accepted offer in hand even faster than this.

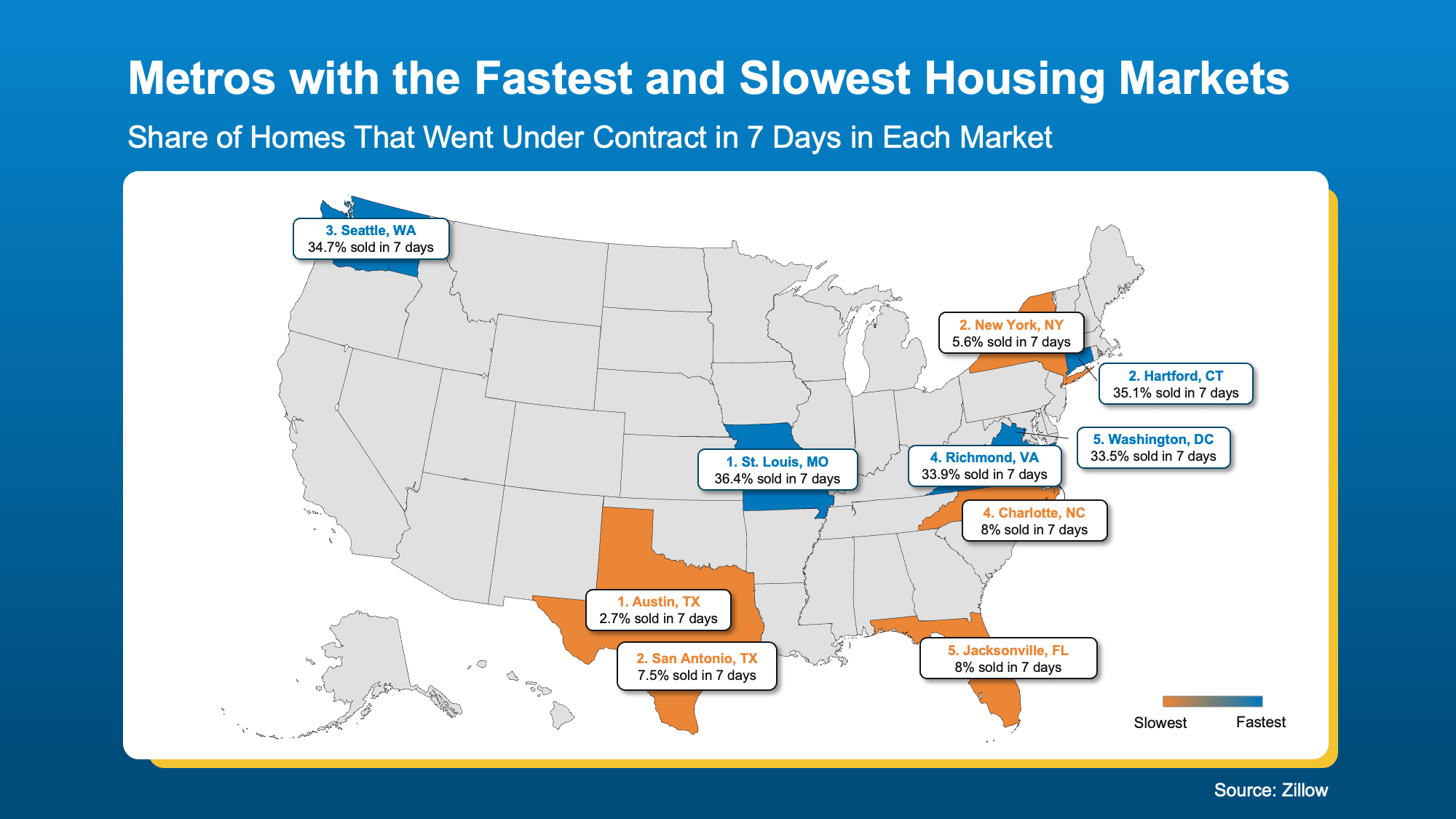

Markets Where Homes Still Sell Quickly, Even Now

Zillow says the typical home will go “pending” or “under contract” in 19 days. Some homes even see it happen in as little as 7 days. It just depends on where you are – and how you prep your house.

So, don’t let the slowing pace of sales stress you out. Homes can still sell fast, if they’re positioned right.

Just to show you, here’s a quick look at some of the markets that are moving faster than the norm, according to Zillow (see map below). This’ll show you how different it can be based on where you live.

The key things you need to remember when looking at this visual:

The key things you need to remember when looking at this visual:

- It varies a lot based on where you live. Within the same state, individual neighborhoods or pockets may sell much faster than the norm.

- Even in slower moving states, you can still sell quickly. As the map shows, in those places there are still homes that go under contract in as little as a week.

So don’t worry about if your state made either list. As Orphe Divounguy, Senior Economist at Zillow, says:

“The cream of the crop is still selling fast, even in markets that have slowed considerably. . .”

The Big Reasons Some Homes Sit, and Some Sell Fast

And here’s the big secret. While location can definitely play a role, it’s not just about location. It’s about strategy.

Today’s buyers are paying attention to condition. They’re comparing photos, upgrades, layout, location, and price. And they’re choosing homes that feel move-in ready and well worth the value.

The homes that check those boxes? They’re not sitting for long – no matter where they are.

As the Wall Street Journal (WSJ) explains:

“. . . some homes are still flying off the shelves. These houses are often in the Midwest or Northeast, where the lack of new construction keeps a lid on supply. Certain homes in other markets are selling quickly, too, often when a home is move-in ready.”

Because in any market – hot or not – if a home is overpriced, needs too much work, or just doesn’t meet current buyer expectations, it’s not going to sell.

In this market, the sellers who win are the ones who get real about their house. They’re honest about how their home compares to other listings, realistic about price, and they work with an agent who truly understands today’s market and what it takes to sell.

When your agent knows how to price strategically, spotlight the strengths of your home, and move quickly when the market gives clear signals, that’s when the results follow.

Bottom Line

Today’s housing market rewards the right strategy. Because even in a slower area, the homes that are priced realistically and positioned well are still selling – sometimes faster than you may expect.

Let’s connect if you’re ready to make yours one of them. Call Liz Norvell at (928) 458-4025.

Wondering If You Should Still Buy a Home Right Now? Here’s What To Keep in Mind.

With economic headlines, global events, and near constant talk about affordability, you may be wondering if this is the right time to move. But here’s what you need to remember.

While recent events do have some impact on the housing market, they don’t take buying off the table. You just have to use a different strategy.

Mortgage Rates Have Been Up Slightly – Here’s Why

After trending down for most of 2025, mortgage rates have been higher again for over roughly a month now. And experts say it’s a result of what’s happening overseas and in the broader economy. As Mark Fleming, Chief Economist at First American, explains:

“Mortgage rates have recently moved higher, driven by geopolitical uncertainty and rising energy costs that are contributing to inflation concerns.”

But what does that really mean for you? Should you wait for everything to settle back down before you buy a home?

The short answer is no. You don’t have to wait.

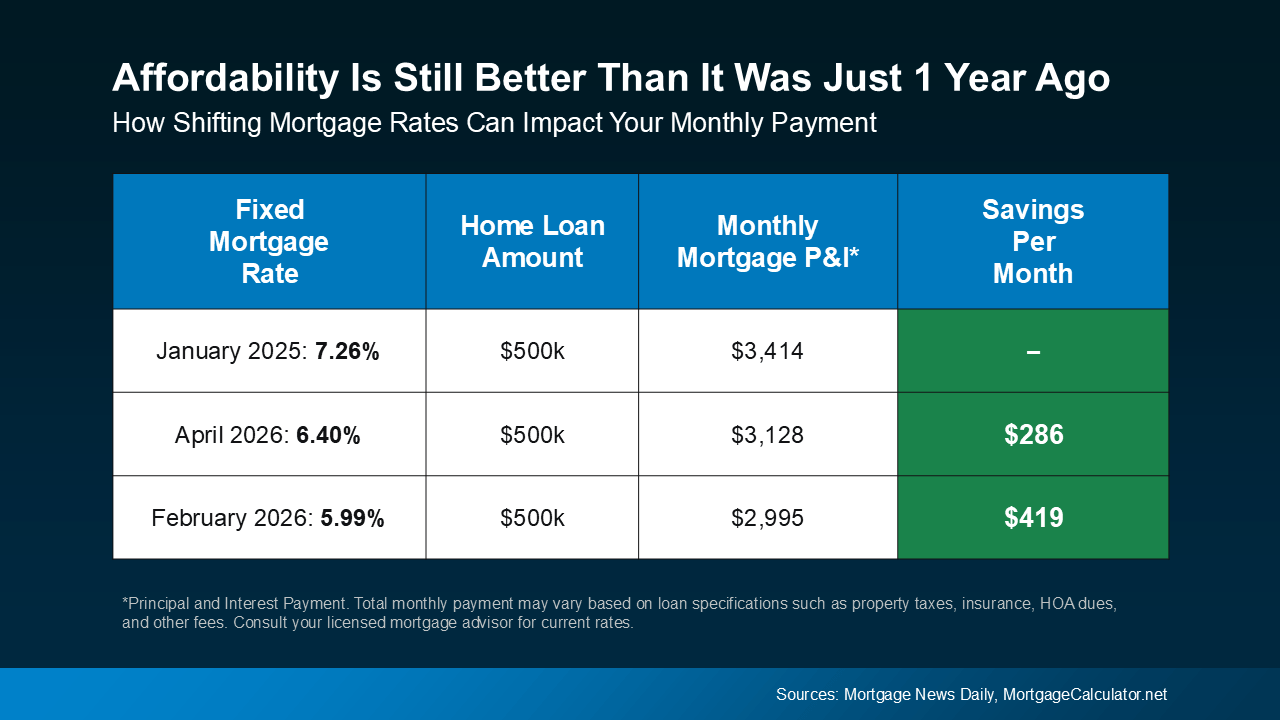

Your Window To Buy Didn’t Close

It’s true that a month or so ago, when rates were just shy of 6%, buying felt a bit more affordable. And now that rates are hovering around the mid-6s, monthly payment costs are higher.

But zoom out for a second.

Let’s say you’re taking out a loan for $500k. Even with rates in the mid 6s, you’re still saving roughly $300 on your monthly payment compared to buyers who made their purchase early last year.

That means this recent increase in rates hasn’t erased the progress we’ve seen. Buying is still more affordable than it was just one year ago (see below):

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

The goal moving forward shouldn’t be to perfectly time the market. Things change too quickly for that. Instead, the real goal is to make the best decision you can based on where things are today. And the best advice anyone can give is: brace for volatility.

When It Comes To Rates, Expect the Unexpected

Mortgage rates are going to continue to be move around in the weeks or months ahead as new information and economic reports come out.

Try to remember, you can’t control global events or where rates go next week (or even next month). But you can control how you prepare. If you do that, it becomes less about the headlines, and more about your situation.

If You Want or Need To Move, You Still Can

The simple truth is, if you want or need to move, you still can.

Some buyers are choosing to move forward right now because their needs haven’t changed. A growing family, a job relocation, a lifestyle shift – those things still matter.

And for buyers who do decide to move forward, there are ways to make it work.

For example, you could explore options like adjustable-rate mortgages (ARMs) to get a lower rate upfront. That may or may not be the right fit for you, but it highlights an important point: there are strategies that can help you move, even now.

What matters most is having a plan.

And working with the right agent and lender is a big part of that. With expert help, you’ll:

- Understand your budget and what the math looks like at today’s rates.

- Explore your financing options, including ARMs and assistance programs.

- Have trusted guidance from experts who’ll keep you up to date throughout the process.

Bottom Line

Even though there’s some uncertainty, that doesn’t mean you’re out of options.

If you need to move, you still can. Let’s connect so we can explore all your options and make your move happen.

![]()

(928) 458-4025

One Key Sign We’re Not Headed for a Wave of Foreclosures

Foreclosures are ticking up. And that may make your mind jump straight to thoughts of 2008 – specifically to what happened to the market during the housing crash. So, let’s do exactly what your brain already wants to do, and see if there’s any connection there.

The simple truth is foreclosure filings are rising. But they’re nowhere near crisis levels. And that’s not where they’re headed either. Here’s why.

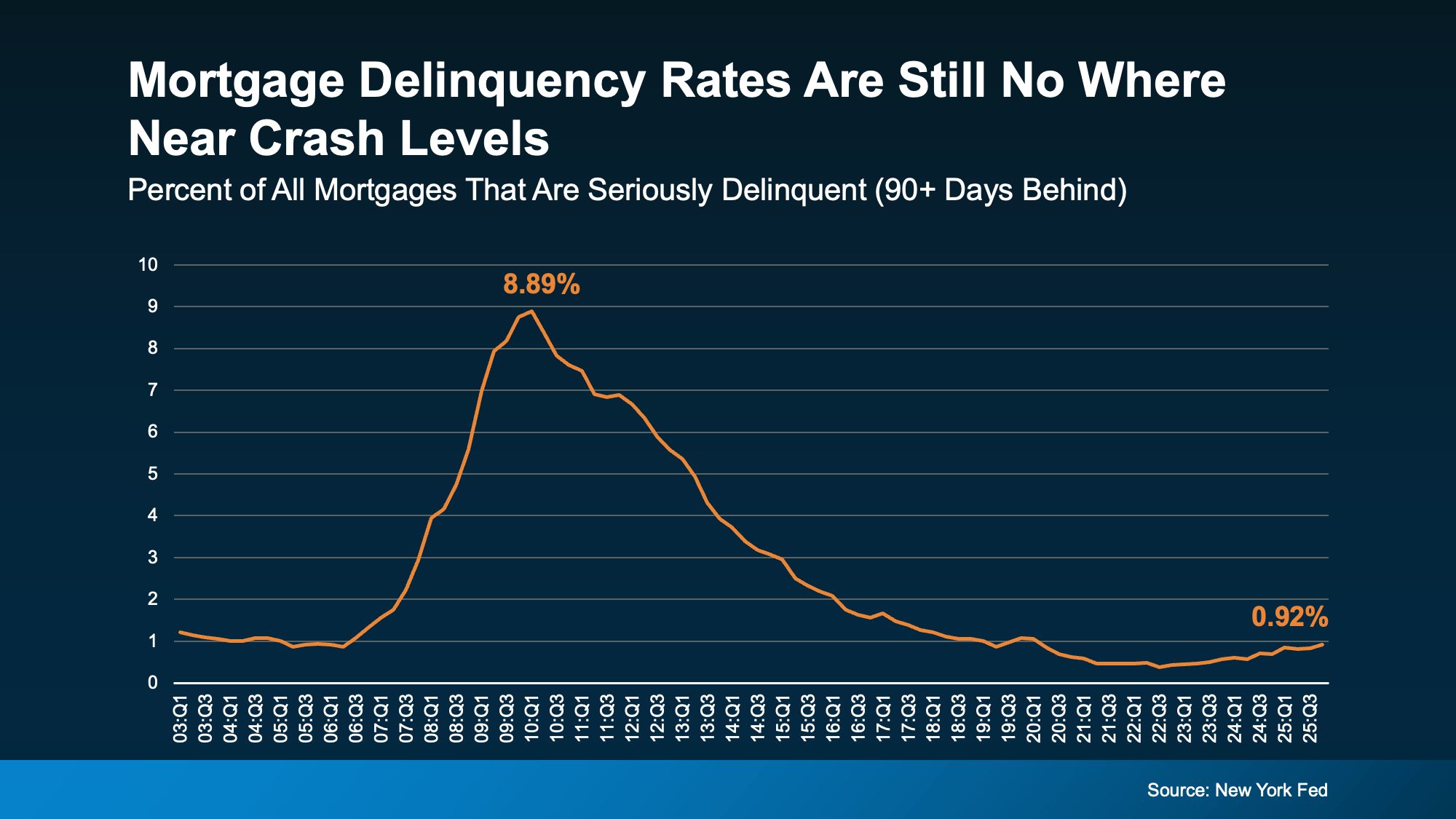

Take a look at serious delinquencies – loans where the homeowner is more than 90 days late on their mortgage payments.

While those have increased slightly, data from the New York Fed shows they still remain low. And they aren’t anywhere close to levels seen when the market crashed (see graph below):

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

In the years around the crash, they were up around 9%. That’s 1 in 11.

That’s a big difference.

And it’s important to remember not all delinquencies even become foreclosure filings. Some homeowners who are falling behind will work out repayment plans with their banks and lenders because banks don’t want to see a wave of foreclosures either.

That’s why foreclosure numbers are even lower than delinquencies. ATTOM shows only 0.3% of all homes are currently going through a foreclosure filing. And those won’t even all go to a full foreclosure. That’s not a wave. That’s a ripple at most.

If People Are Falling Behind on Payments, Why Aren’t There Even More Foreclosures?

And maybe you’re wondering, if people are struggling financially, why aren’t there more foreclosures? Here’s the easiest way to answer that.

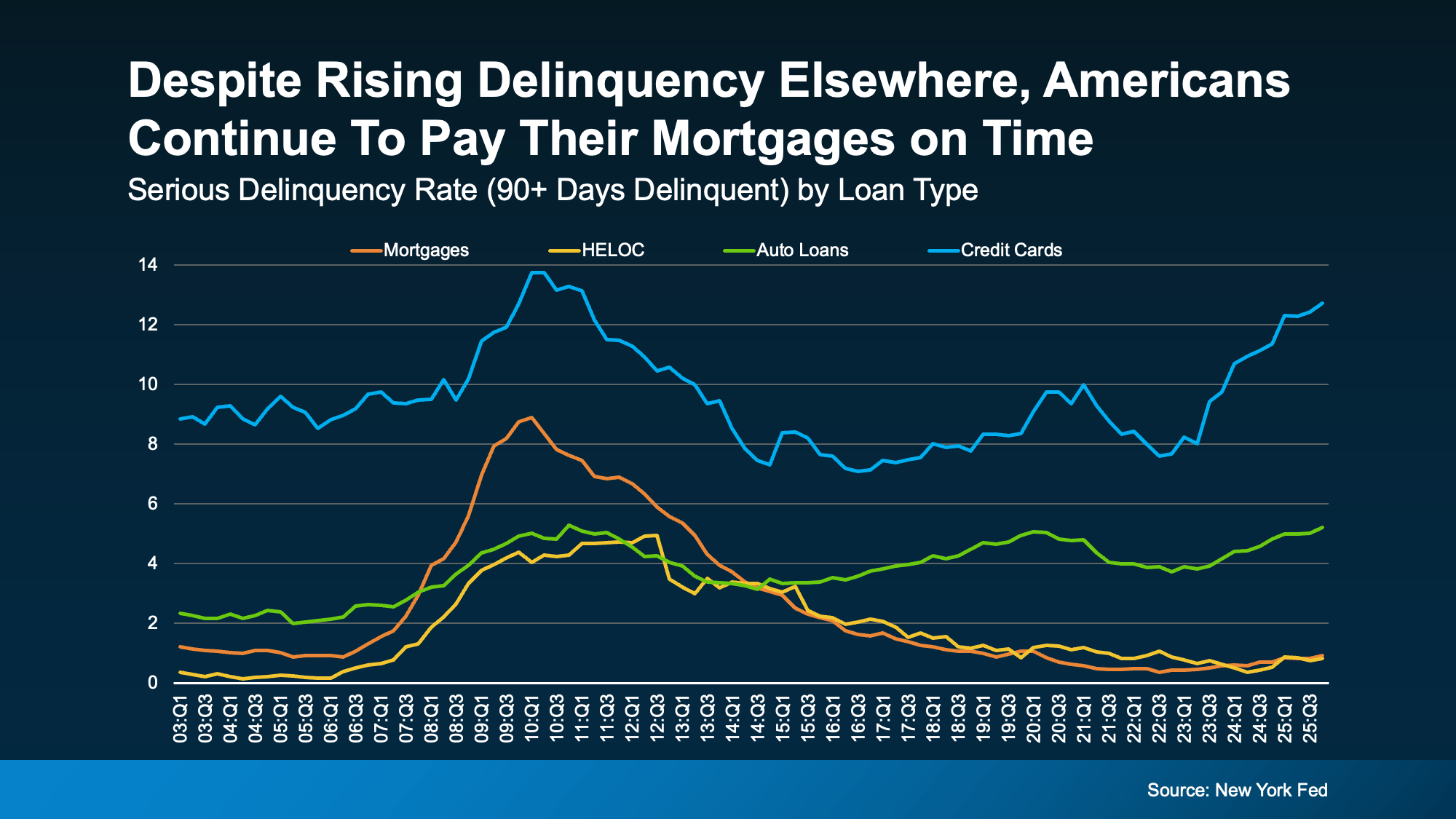

When households feel financial pressure, they tend to prioritize their mortgage payment above almost everything else. Because the last thing they want to lose is their home.

Data from the New York Fed shows serious delinquencies have risen more for credit cards and auto loans (the blue and green lines). But mortgage delinquencies and home equity lines of credit (borrowing against the value of your home) aren’t seeing the same big uptick (the yellow and orange lines). They’re a lot more stable overall.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

Home Equity Changes Everything

Many people have built significant equity over the past several years. And that creates options. As Daren Blomquist, VP of Market Economics at Auction.com, explains:

“Distressed homeowners… many times they still have equity in their homes. There’s an opportunity for them to sell that home, avoid foreclosure, and walk away with equity.”

That’s a major difference from 2008. Back then, many homeowners owed more than their homes were worth. And selling wasn’t an easy solution. Today, for many people, it is. And even in situations where equity isn’t enough, homeowners are encouraged to contact their loan servicer early to explore alternatives to foreclosure.

Bottom Line

Are foreclosure filings rising slightly? Yes. Are they anywhere near crash territory? No. And homeowners today have far more equity and flexibility than they did during the crash.

If you’re concerned about what you’re seeing in the headlines, the best move isn’t panic, it’s perspective. And the data right now says this isn’t 2008 all over again.

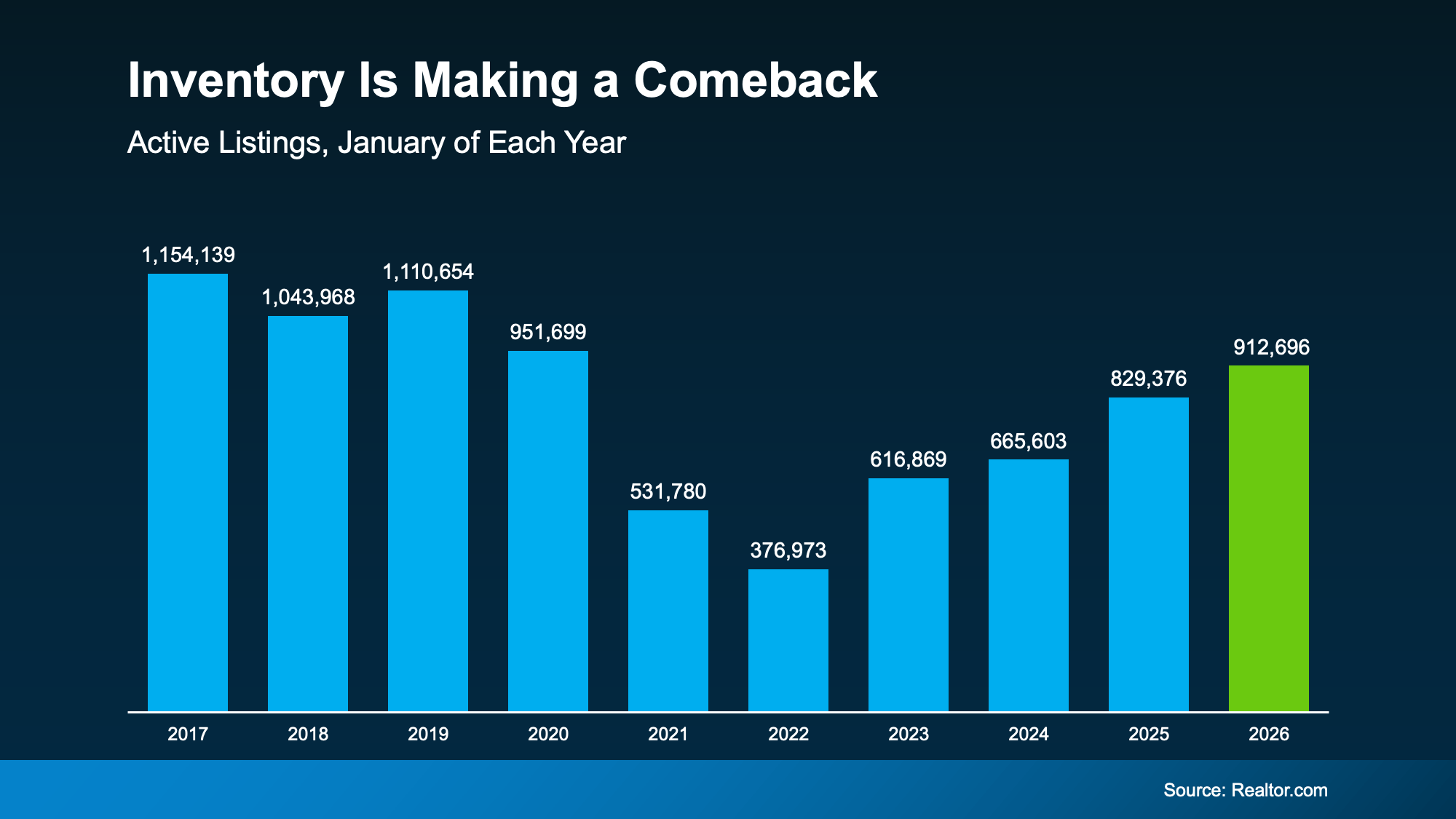

Inventory Is Making a Comeback in 2026

After a long stretch where buyers were competing for too few homes, inventory has made a comeback over the past year. And depending on where you live, that’s opening up your options in a meaningful way.

According to Realtor.com, the number of homes available for sale in January was the highest it’s been since 2020. Here’s why that’s such a big deal. Getting back to pre-pandemic levels signals a slow and steady return to what’s typical:

Now, it’s worth noting, nationally we’re not there yet – and having more inventory improving won’t suddenly “fix” the market. But the growth we’ve seen lately still changes how competitive the market feels.

- When there are more homes for sale, buyers gain time, options, and leverage.

- When there aren’t, the pressure ramps up quickly.

In the years since 2020, there weren’t enough homes for sale, and that made the market feel different. Rushed. Stressful. Intimidating.

But now it’s finally getting better.

A Growing Portion of the Country Is Getting Back to Normal

Depending on where you live, inventory growth is going to vary. Some places are bouncing back faster than others. According to Lance Lambert, Co-Founder of ResiClub, in January 2025, just a little over one year ago, only 41 of the 200 largest metros were back to normal inventory-wise.

But around the end of year, almost half (90) of the largest 200 metro areas were back at or above typical levels. That’s a big improvement in roughly a year. And it’s not done yet.

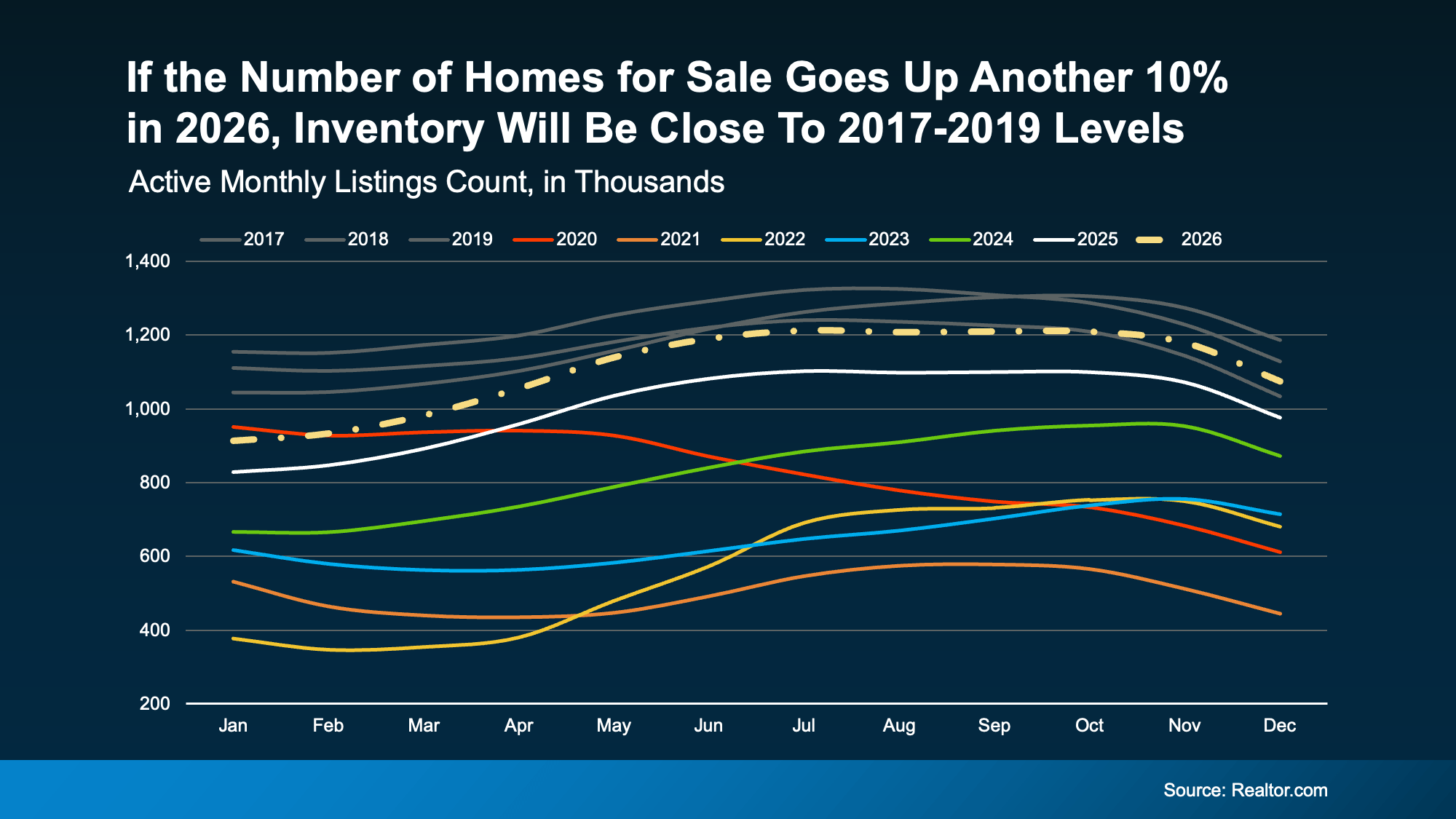

Inventory Is Expected To Keep Growing

Looking ahead, forecasts suggest the number of homes for sale could rise another 10% this year, which means even more markets should join the list of places where supply has rebounded.

Here’s a graph that shows what an extra 10% would do for the market this year. You can see that projected growth (shown in the dotted line) hits inventory levels seen in 2017-2019 by roughly this fall (the gray lines). That means we may reach normal by end of year, nationally:

And that changes your home search in a good way. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, puts it:

“. . . housing market conditions are gradually rebalancing after several years of extreme seller advantage. Buyers are beginning to see more options and modest negotiating power as inventory improves . . .”

In other words, the market is starting to work with buyers again — not against them.

Bottom Line

Inventory isn’t fully back to normal everywhere. But it’s moving in the right direction. And, in some areas, it’s already there.

If you’ve been waiting for a moment when you have options and a little breathing room, this is the strongest setup buyers have seen in a long time.

If you want to know what’s happening in our local market, let’s talk.

Liz Norvelle

(928) 458-4025

![]()

Not Sure If You’re Ready To Buy a Home? Ask Yourself These 5 Questions.

But here’s what you need to remember. While housing market conditions are definitely a factor in your decision, your own personal situation and your finances matter too. As an article from NerdWallet says:

“Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”

So, instead of trying to time the market, focus on what you can control. Here are a few questions that can give you clarity on whether or not you’re ready to make your move.

1. Do you have a stable job?

Buying a home is a big commitment. You’re going to take out a home loan stating you’ll pay that loan back. Knowing you have a reliable job and a steady stream of income is important and will give you peace of mind for a purchase so large.

2. Have you figured out what you can afford?

If you have a reliable paycheck coming in, the next thing to figure out is what you can afford. This depends on your budget, spending habits, debts, and more.

At this point, it helps to talk with a trusted lender. They’ll be able to tell you about the pre-approval process and what you’re qualified to borrow, current mortgage rates and your approximate monthly payment, closing costs, and other expenses you’ll want to budget for. That way, you have a good idea of what to expect.

3. Do you have an emergency fund?

As you crunch your numbers, you’ll want to make sure you have enough cash left over in case of emergency. Think about it. You don’t want to overextend on the house, and then not be able to weather a storm if one comes along. It’s not a fun topic, but it’s an important one. As CNET says:

“You’ll want to have a financial cushion that can cover several months of living expenses, including mortgage payments, in case of unforeseen circumstances, such as job loss or medical emergencies.”

4. How long do you plan to live there?

It was mentioned above, but buying a home comes with some upfront expenses. And while you’ll get that money back (and more) as you gain equity, that process takes some time. If you plan to move again soon, you may not recoup your full investment.

So, how long should you stay put in an ideal world? Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Five years is a good, comfortable mark. If the price of your home appreciates considerably, then even three years would be fine.”

So, think about your future. If you’re going to live there for a while, it may make sense to go for it. But, if you’re looking to sell and move within a year or two because you’re planning to transfer to a new city with that promotion you’ve been working so hard for, or you anticipate you’ll need to move to take care of family, those are things to factor in.

5. Do you have a team of real estate professionals in place?

If you do, great. But if you don’t, finding a trusted local agent and a lender is a good first step. Having the right team can make figuring out everything else easier. The pros can talk you through your options and help you decide if you’re ready to make your move, or if you have a few more things to get in order first.

Bottom Line

If you want to have a conversation about the most important things you need to consider when buying a home, let’s connect.

928-458-4025

Why You Don’t Need To Be Afraid of Today’s Mortgage Rates

Mortgage rates have been the monster under the bed for a while. Every time they tick up, people flinch and say, “Maybe I’ll wait.” But here’s the twist. Waiting for that perfect 5-point-something rate could end up haunting your wallet later.

The Magic Number

According to the National Association of Realtors (NAR):

“. . . a 30-year fixed rate mortgage of 6% would make the median-priced home affordable for about 5.5 million more households—including 1.6 million renters. If rates were to hit that magic number, it’s likely that about 10%—or 550,000—of those additional households would buy a home over the next 12 or 18 months.”

When the market hits that mortgage rate sweet spot, as expert forecasters are starting to say is more likely in 2026, the psychological shift to lower rates will kick in for more of today’s hopeful buyers. That will unleash some pent-up demand that’s been waiting on the sidelines, and the increase in activity will cause prices to rise.

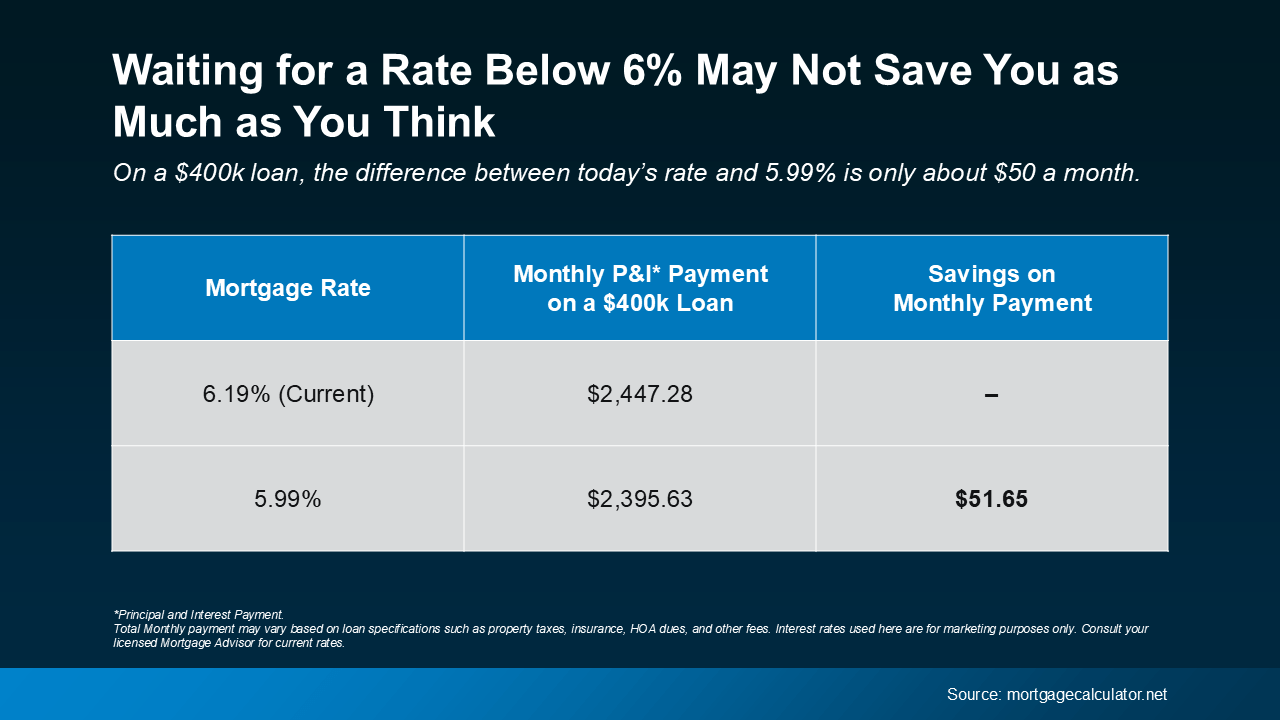

And while a 5.99% rate might sound like a big win, if you’re waiting for that number to make your move, it might not actually save you as much as you think. Here’s how the math looks when you run the numbers (see chart below):

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

So, if you’re waiting for 5.99%, that difference might not be worth missing out on today’s opportunities, like having more homes to choose from, better negotiation leverage with today’s sellers, and fewer buyers out there looking for the same houses.

Because the reality is, those benefits start to slip away when more buyers begin to make their moves – and a rate under 6% is exactly they’re waiting for.

Why Acting Now Makes Sense

Jessica Lautz, Deputy Chief Economist and VP of Research at NAR, says:

“Over the last 5 weeks, mortgage rates have averaged 6.31%. This has provided savvy buyers a sweet spot to reexamine the home search process with more inventory, widening their choices.”

And like Matt Vernon, Head of Retail Lending at Bank of America, notes:

“Rather than waiting it out for a rate that they like better, hopeful homebuyers should assess their personal financial situation—if the house is right for them, and the upfront and monthly payments are affordable, it could be the right chance to make a move.”

Bottom Line

If moving at today’s rate scares you, remember, waiting doesn’t always pay off. Once rates dip below 6%, as some experts project they’ll do next year, more buyers (and higher prices) will be back.

So, don’t be afraid of today’s mortgage rates. Because if you’re ready, this might just be your chance to make your move before the market wakes up again.

![]()

(928) 458-4025

Top 10 Tips to Sell Your Home Faster

Selling your home quickly and for the best price is all about thoughtful preparation. With a focused strategy, you can attract serious buyers and move toward a successful closing in record time. Here are ten practical tips to help you prepare your property for a fast sale.

1. Price It Right From the Start

Set your price based on a thorough analysis of comparable homes (or “comps”) that have recently sold in your area. Overpricing can scare away buyers and leave your home sitting on the market, so work with your agent to find that sweet spot that reflects actual market value.

2. Boost Your Curb Appeal

First impressions are everything. Make buyers fall in love before they even step inside by power washing siding, cleaning windows, and planting fresh flowers. A new welcome mat and a freshly painted front door are impactful yet effective touches.

3. Handle Repairs and Consider a Pre-Inspection

Address any nagging issues, such as leaky faucets, cracked tiles, or broken light fixtures. Completing a pre-listing inspection can also reveal hidden problems, allowing you to address them upfront and offer buyers total peace of mind.

4. Declutter and Depersonalize Your Space

Help buyers envision themselves living in your home by packing away personal photos, collections, and excess furniture. Clearing countertops and organizing closets makes your space feel larger, cleaner, and more inviting.

5. Stage for Maximum Appeal

Arrange furniture to highlight your home’s best features and improve flow from room to room. Proper staging helps define each space and shows buyers how they can utilize it, transforming empty rooms into functional and appealing areas.

6. Invest in Professional Photos and Video

Most buyers start their search online, making high-quality visuals essential. Professional photos and a video tour will make your listing stand out, capturing your home’s best angles and attracting more showing requests.

7. Be Flexible with Showings

The more people who see your home, the faster you’ll get an offer. Try to accommodate as many showing requests as possible, including those on evenings and weekends, to make it easy for potential buyers to visit.

8. Write a Compelling Listing Description

Work with your agent to craft a description that tells a story. Highlight key features, such as a new kitchen or a spacious backyard, and mention nearby amenities like parks, excellent schools, or popular cafes to showcase the complete lifestyle.

9. Create a Strategic Launch Plan

Timing is key to generating buzz. Plan to list your home later in the week to capture the attention of weekend house hunters and consider holding an open house on the first weekend to create a sense of urgency.

10. Prepare for Negotiations

When an offer comes in, please review it carefully with your agent. A strong offer is about more than just price; look for buyers with pre-approval letters and minimal contingencies to ensure a smoother, faster closing process.

Ready to put these tips into action? Call me, together we can sell your house quickly! Liz Norvelle 928-458-4025

Stage Your Garage: A Seller’s Guide to a Faster Sale

When you prepare to sell your home, you likely focus on the kitchen, bathrooms, and curb appeal. But what about the garage? Many sellers overlook this space, treating it as a last-minute dumping ground for clutter. A well-staged garage can be a powerful selling point that helps your home sell faster and for a better price.

Potential buyers see a clean, organized garage not just as a place to park cars, but as valuable, usable square footage. It shows them the home has been well-maintained and offers possibilities for hobbies, storage, and more. This guide provides a practical, step-by-step plan to transform your garage from a forgotten space into a feature that wows buyers.

Garage Staging Process

Step 1: Declutter, Sort, and Dispose

The most crucial step is ruthless decluttering. The goal is to empty the garage by at least 50% to create a sense of spaciousness.

The Four-Box Method

Set up four distinct areas or use large bins labeled:

- Keep: Items you use regularly and will take to your new home. Be strict. If you haven’t used it in a year, it probably doesn’t belong here.

- Donate: Items in good condition that can benefit others. Think old tools, sports gear, or furniture.

- Sell: Higher-value items you don’t need. Consider online marketplaces, consignment shops, or a garage sale.

- Trash/Recycle: Broken items, expired chemicals, and anything unusable.

Handling Unwanted Items

Properly disposing of items is key.

- Donations: Local charities such as Goodwill, Salvation Army, or Habitat for Humanity ReStore are excellent options. Some offer pickup services for larger items.

- Disposal: For hazardous materials such as old paint, pesticides, or motor oil, check with your local municipality to find designated hazardous waste drop-off days or facilities. Never pour these down the drain or put them in regular trash. For large amounts of junk, consider renting a small dumpster for a weekend.

Step 2: Smart Storage Solutions

Once decluttered, the goal is to get as much as possible off the floor. Vertical and overhead storage make the garage look larger and more organized.

Vertical Wall Storage

- Open Shelving: Sturdy, freestanding metal or plastic shelving units are affordable and effective. They allow you to neatly stack bins.

- Pegboards: A classic for a reason. Pegboards are perfect for hanging tools, gardening equipment, and small items, keeping them visible and accessible.

Overhead Ceiling Racks

Don’t forget the space above your head. Ceiling-mounted racks are ideal for storing items you don’t need often, such as holiday decorations or camping gear.

Cohesive Containers

Invest in a set of matching, opaque storage bins with lids. Clear bins can look cluttered. Using uniform containers creates a clean, intentional look. Label each bin clearly so buyers (and you) know the space is functional.

Step 3: High-Impact, Low-Cost Upgrades

A few cosmetic and functional improvements can dramatically elevate your garage’s appeal without breaking the bank.

Refresh the Floor

A stained, cracked concrete floor can make the whole garage feel grimy.

- Epoxy Floor Coating: This is the gold standard. An epoxy coating provides a durable, glossy, and easy-to-clean surface that resists stains. It makes the entire space feel finished and professional.

- Interlocking Floor Mats: A less permanent but still effective option. These mats can cover imperfections and add a clean, patterned look.

Improve the Lighting

Most garages are equipped with a single, dim bulb. Buyers respond to bright, well-lit spaces.

- Upgrade Fixtures: Replace bare bulbs with bright, energy-efficient LED shop lights. They provide even, daylight-quality light, making the garage feel safer and more inviting.

Quick Cosmetic Fixes

- Patch and Paint: Fill any holes or cracks in the drywall. Apply a fresh coat of neutral-colored paint (like a light gray or beige) to the walls. This simple step can make the garage feel 100% cleaner and brighter.

- Update Hardware: Replace old, rusty cabinet handles or light switch covers. It’s a small detail that contributes to a fresh look.

- Label Everything: Use a label maker to mark shelves, bins, and cabinets. This reinforces the theme of organization and shows buyers the space is thoughtfully designed.

Preparing for Photos and Open Houses

For professional photos and buyer showings, the garage should be pristine.

- Park Cars Elsewhere: Always remove cars from the garage for photos and viewings. This makes the space look as large as possible.

- Open the Door: Let in natural light by opening the garage door during daytime showings.

- Turn on All Lights: Showcase your new, bright lighting.

- Final Sweep: Do one last sweep to remove any dust, cobwebs, or debris.

By investing a little time and effort into your garage, you do more than clean up a messy space. You present a complete, well-maintained home that allows buyers to see its full potential, helping you secure a top-dollar offer in record time.